Salesforce: An ever-expanding TAM and a new focus on operating margins

The market has always had a love/hate relationship with Salesforce. On one end, you have a business that has been able to grow revenue sustainably for decades, albeit with some assistance from M&A — notably Tableau, Mulesoft, and Slack. On the other end, it’s a software business trading at 10X sales when other SaaS businesses are comfortably trading between 20-50x sales.

This is probably the result of a few things:

1) There’s been a notable lack of margin expansion as revenue has scaled materially

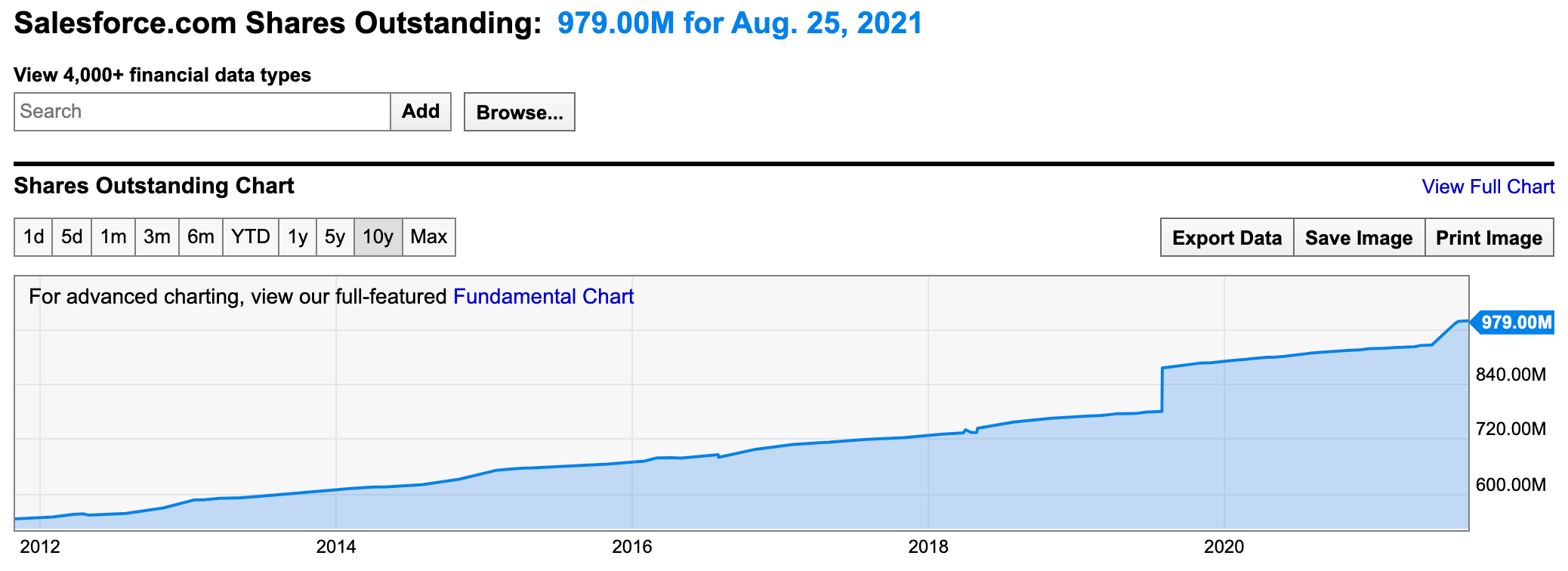

2) A focus on M/A and inorganic growth and as a result a neverending increase of its share count

The M&A Model

While the market may not appreciate Salesforce’s latest acquisitions, particularly the price paid for Slack, there’s little doubt that Tableau, Mulesoft, and Slack have been major successes for Salesforce.

Platform, which is comprised of Tableau, Mulesoft, and Slack, now represents the largest segment of their business and is growing at 24% a year, faster than the flagship Sales cloud.

In the most recent earnings call, Salesforce called out Tableau and Mulesoft:

Slack itself grew 39% on a stand-alone basis.

Salesforce Customer 360 strategy of having customers adopt more clouds is working

As a result of their M&A model, Salesforce has seen its TAM continually rise

Breaking down the acquisitions:

1) Mulesoft was acquired in 2018 for $6.5B at 22X sales. It’s hard to find specifics, but there’s some indication that Mulesoft is now over a $1.5B revenue run rate growing around 50%. That means Salesforce acquired it at a little more than 4x current revenue.

2) Tableau was acquired in 2019 for $15.7B. As far as I know, Salesforce has only disclosed Tableau quarterly revenue once, in the April 2020 quarter, and it was $285M though not growing fast. That’s a ~$1.2B revenue run rate, meaning Salesforce acquired it for 13x current revenue. (These are estimate, please correct me if I’m wrong)

3) Slack was acquired for $26.79B in December 2020. This one is most recent and Slack recently announced it is at a $1B revenue run rate but growing over 40%.

The opportunities going forward

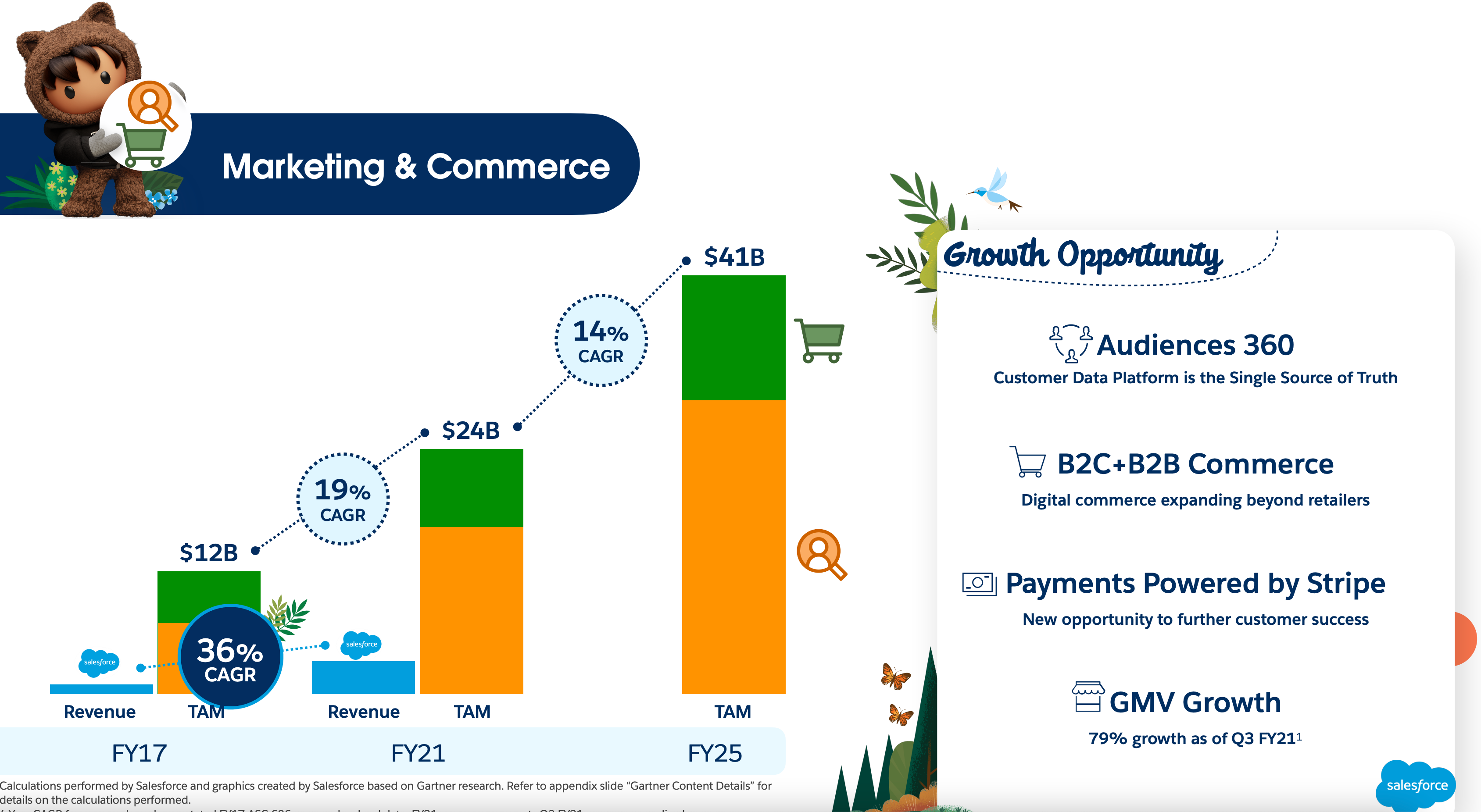

In their investor presentation, Salesforce highlights the growing opportunities within each segment, with the TAM of their “Marketing & Commerce” segment expected to compound at 14% over the next 4 years. Keep in mind that while the TAM increased 19% the last 4 years, Salesforce itself has compounded revenue in this segment at 36%, roughly twice the market rate.

While the TAM for Platform has compounded at only 3% in the last 4 years, Salesforce has compounded Platform revenue at 25% and forsees that the TAM compounds at 7% in the next 4 years.

A new focus on operating margins

The highlight of Salesforce’s most recent earnings call, at least for the market, was the emphasis placed on a new, more disciplined approach and a focus on operating margins. The phrase “operating margins” was used over 20 times in the call by CEO Mark Benioff and CFO Amy Weaver, more than quadruple the number of times it was mentioned on the call 2 quarters ago.

The stock

The stock is not terribly expensive here, and while I’ve written before that I don’t do complex valuation and models, my thinking around Salesforce valuation is even simpler. If you think operating margins are going to be around 30-35% at maturity, that means P/S will be around 10 (where it is now), which also means that the returns from here will simply be in line with revenue growth. It’s not hard to see Salesforce continuing to grow revenue 15-20% for another 5 years at least.